So on July 4, 2025, President Trump signed the One Big Beautiful Bill—yeah, they really called it that—into law. And look, I get it. Tax reform is boring. But this one? It actually touches your life in ways that matter.

Whether you're running a side hustle, trying to keep a small business afloat, saving for your kid's college fund, or just trying to figure out why half your freelance budget is disappearing to overseas contractors, the OBBB changed the game. Some of it's genuinely good news. Some of it? Well, let's just say you're gonna want to know about it before tax season hits.

The Real Talk

Here's the thing about tax bills: politicians love to call them "tax cuts" or "relief packages," but what they really mean is "here's who wins and here's who pays." The OBBB is no different. It's got some solid wins for regular people—especially if you're a server, a small business owner, or a parent trying to save for your kid's future. But it also has some sneaky stuff buried in there that's gonna cost you if you're not paying attention.

This isn't the usual "here's the technical breakdown" article. This is the real-world version. We're talking actual numbers, actual examples, and actual strategies for making sure this bill works for you instead of against you.

Let's dig in.

What Even IS the One Big Beautiful Bill?

Okay, so here's the deal: the "One Big Beautiful Bill"—or OBBB if you're into acronyms—is Congress's latest attempt to overhaul the tax code and make it "simpler and fairer." (Spoiler alert: it's still complicated, but at least they tried.) Officially, it's Public Law 119-21, signed into law on July 4, 2025. And yeah, they really did sign a massive tax reform bill on Independence Day. Symbolism much?

The OBBB is basically a major rewrite of the Internal Revenue Code—that thick, confusing rulebook that's been making accountants rich since forever. Think of it as the sequel to the 2017 Tax Cuts and Jobs Act, but with some new plot twists. Instead of just tweaking rates here and there, the OBBB actually restructures how taxes work for individuals, families, small businesses, and anyone making money outside a traditional 9-to-5 job.

Here's what makes it different from previous tax reform: it's not just about lowering rates (though it does some of that). It's about changing what gets taxed in the first place. Tips? No longer taxable. Overtime pay up to a certain limit? Tax-free. Money you put into a new savings account for your kids? Potentially tax-advantaged. It's a fundamental shift in how the IRS thinks about what counts as "income" and what counts as "stuff we're not gonna tax."

The bill came out of a Republican-controlled Congress and the Trump administration's push to simplify the tax code and put more money back in people's pockets—or at least, that's the pitch. But like any tax bill, the devil's in the details. Some people win big. Some people get hit with unexpected costs. And some people (looking at you, freelancers using Fiverr) didn't see it coming at all.

The OBBB touches nearly every part of the tax code: individual income taxes, business deductions, retirement savings, education savings, investment rules, and even international payments. It's the kind of bill that affects whether you pay taxes on your tips, how much you can deduct from your business expenses, whether your kid's college fund gets a tax break, and—this is the kicker—how much it costs to hire someone overseas to do work for your company.

In short: the OBBB is a big, sweeping rewrite of the rules. And whether it's good or bad for you depends entirely on your situation. That's why we're here—to break down what actually changed and what it means for your wallet.

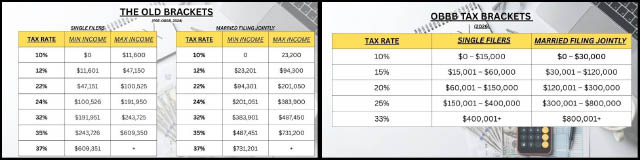

The Pragmatic Truth About These Tax Brackets

Let’s be honest: tax brackets are only part of the story, and “simpler” doesn’t automatically mean “fairer.” Sure, the OBBB trimmed the number of brackets from seven to five and nudged some rates down, but the real game is who’s actually paying the tab—and spoiler, it’s still the middle class doing most of the heavy lifting.

Old Brackets vs. New Brackets: What’s Really Different?

Married brackets are basically the same, just doubled.

On paper, the brackets are wider and the top rate is lower. But here’s the catch: most Americans are in the middle, and that’s where the government collects most of its revenue. The rich have loopholes, the poor get credits, but the middle class? They’re the reliable ATM.

The Real Impact

The new bill significantly increases the standard deduction to encourage simplified filing. However, it also eliminates the personal exemption.

- Middle-Income Earners: You might save a few hundred bucks a year, thanks to wider brackets and a higher standard deduction. But don’t expect a life-changing windfall. The IRS still gets its cut, and you’re still the backbone of the tax system.

- High Earners: Congrats, you get a rate drop from 37% to 33%. That’s real money if you’re in that club, but let’s face it, most folks aren’t.

- Lower-Income Earners: Not much changes. You’re still in the lowest bracket, and credits/deductions do more for you than the bracket itself.

- Small Business Owners: The 23% pass-through deduction is the real win here. If you’re self-employed, this could save you thousands—finally, a break for the folks hustling on their own.

The Broader Reality

Taxes aren’t just about brackets—they’re about deductions, credits, what counts as income, and, honestly, who’s got the best accountant. The OBBB makes things look neater, but the middle class still carries the load. The government needs revenue, and it’s not coming from the ultra-rich or the very poor. It’s coming from everyone in between—the families, the small business owners, the folks who don’t have offshore accounts or fancy trusts.

So yes, you might pay a little less.

But let’s not pretend the weight of the tax system has shifted off the middle class. It hasn’t—and probably won’t.

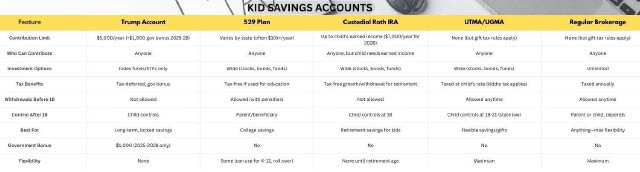

Trump Accounts: Free Money for Babies… with a Big, Fat Asterisk

Let’s cut through the hype: Trump Accounts are the government’s shiny new “savings” product for kids, pitched as a way to kickstart generational wealth. Sounds great, right? Who doesn’t want a free $1,000 for their newborn? But, as with all things “free,” there’s fine print—and it’s basically the financial version of locking your cash in a safe and throwing away the key for almost two decades.

What’s the Deal?

What is it? A kid’s-only savings account (think IRA for babies) with a $1,000 government bonus if your child is born between 2025–2028. You can toss in up to $5,000 a year from all sources, and the money grows tax-deferred.

How do you get it? You have to file special paperwork in mid-2026—miss it, and you’re out of luck.

When can you touch it? Never! The child will have access to it when he or she turns 18. No exceptions. Not for emergencies, not for college for that oldest kid, not for anything.

Who owns it? The child. You’re just the babysitter until they’re 18, then they can blow it all on whatever they want.

Is It a Good Deal?

Let’s be real: if you’ve got a newborn and you’re offered $1,000 for doing a little paperwork, take it. Compound growth is your friend, and if you max out contributions every year, you could end up with a small fortune by the time your kid hits adulthood. Plus, low fees and autopilot investing in index funds mean you’re not losing much to Wall Street middlemen.

But—and it’s a big but—this account should never be your main savings vehicle. Why?

Because:

Zero flexibility: Life happens. If you need the money before your kid turns 18, too bad. It’s locked up tighter than a drum.

Kiddie tax trap: When your kid withdraws the money, the IRS taxes the earnings at your rate, not theirs. So if you’re doing well, you could lose thousands to taxes you didn’t expect.

You lose control at 18: Once your kid’s an adult, it’s their money. Whether they invest it in a startup or spend it all on a spring break trip to Cancun, you have zero say.

Limited investment options: Only index funds and ETFs. No teaching your kid about stock picking, no bonds, no crypto—just the financial equivalent of eating plain oatmeal every day.

The clock is ticking: The $1,000 bonus is only for kids born 2025–2028. After that, it’s just another locked savings account.

My Take

Honestly? Trump Accounts are a decent secondary savings tool—especially if you’re starting from day one with a newborn. Free money is free money, and if you’re disciplined and don’t need flexibility, it’s a fine way to build a little nest egg for your kid. But as a primary savings account? Hard pass. The downsides—especially the lack of access and the tax gotchas—are just too much if you’re hoping to use this for anything other than a long-term, “set it and forget it” play.

If you want flexibility, control, or the option to help your kid with college, emergencies, or launching their first business before age 24, look elsewhere (hello, 529s, Roth IRAs, or even a regular brokerage account). Trump Accounts are the financial equivalent of a time capsule: cool to open in 18 years, but useless until then.

No Tax on Tips: Who’s Actually Winning Here?

Let’s not sugarcoat it—this is a legit win for anyone hustling in the service industry. For the first time ever, tips are 100% tax-free under the One Big Beautiful Bill. That means the money you get slipped under the table, or added to your Venmo, or dropped in your jar, is finally yours to keep—no IRS hand in the till.

Who Qualifies?

- Tipped Employees:

- Restaurant servers, bartenders, delivery drivers, valets, baristas, hotel staff—basically anyone who gets tipped as part of their job. If it’s considered a “tip” by the IRS, you’re in.

- Hourly workers with overtime:

- Up to $12,500 a year in overtime pay is also tax-free. After that cap, normal tax rules apply.

- Retirees:

- If you’re 65+ and collecting Social Security, you get a $6,000 deduction off your benefits before any tax is calculated.

Who Doesn’t Qualify?

- Freelancers:

- Sorry, gig workers—unless your “tip” is truly a gratuity (like a bonus on top of your invoice and clearly marked as such), you’re not off the hook. Most freelance income is still regular taxable income. If you’re a freelance artist and someone “tips” you $20 on top of a $200 project, that $20 might be tax-free if it’s clearly a tip. But if it’s just part of your invoice, it’s taxable.

- Salaried employees:

- No dice. If you’re on a straight salary with no tip income, this doesn’t apply to you. Your bonus? Still taxed. Your commission? Still taxed. This is about classic, service-industry tips only.

- Gig app workers:

- If you’re driving for Uber or DoorDash and get tips through the app, those count as tips and are tax-free. But your base pay from the app? Still taxable.

The Limits & Fine Print

- Overtime Cap:

- Only the first $12,500 in overtime pay is tax-free. Anything above that? Back to normal tax rules.

- Tips Must Be Reported

- No Double-Dipping

The Pragmatic Take

This is a rare, real benefit for working-class folks who rely on tips and overtime. For everyone else—freelancers, salaried workers, and most gig economy types—it’s business as usual. The IRS giveth, but only to a very specific crew.

Bottom line: If you’re in the service industry, celebrate. If you’re not, don’t get cute with your invoicing—the IRS knows the difference.

If You Ignore the Math and Remember Your Talking Points...

That leaves us somewhere between “well, that’s something” and “is this really the best we can do?”

Take the Trump child accounts. On paper, it sounds great: $1,000 for every new baby born in the right window. For anyone staring down hospital bills, formula prices, and the cost of simply being alive in 2026, that’s real money.

But here’s the twist: parents never actually see it. The money sits there until the kid turns 18—at which point they cash it out and get smacked with the tax bill. You can’t tap it for an emergency. You can’t redirect it if life goes sideways. The “investment” is locked in a government-designed box and then handed, all at once, to an 18-year-old in a world where even fully grown adults struggle with basic financial decisions.

Meanwhile, we already have flexible ways to build wealth for kids: 529 plans, custodial accounts, regular investment vehicles, and private options that can be tailored to how real families actually live. Many of those offer similar or better long-term benefits—without the one-size-fits-all, hope-your-kid-doesn’t-blow-it-at-18 structure.

So the Trump child accounts, they start to look less like a bold new frontier and more like a very specific coupon: redeemable only at one store, under certain lighting, between 2:00 and 2:15 p.m. Nice if you happen to be standing in the right place at the right time—but not exactly a serious answer to structural problems. And no, no one is rearranging their reproductive schedule for, $1,000 they’ll never touch.

The same vibe runs through the no-tax-on-tips and Social Security wage pieces. If you live on tips or lean heavily on Social Security, keeping more of every dollar is genuinely helpful. That’s not nothing. But if your income is a messy mix of W-2s, gigs, side hustles, freelance checks, and “whatever pays this month’s bills,” the relief is so targeted it borders on selective. Helpful? Sure. Transformative? Only if your life fits the fine print.

All of this is playing out in an economy that’s officially “strong” but feels anything but. Wages chase prices. Debt shadows paychecks. People stack jobs, hustle on the side, and still wonder why doing everything “right” doesn’t add up the way it was supposed to.

So yes, this bill has some shiny parts. The $1,000 baby boost will help a slice of new parents save. The tax breaks on tips and Social Security will give certain workers a little more breathing room. But it’s hard to escape the sense that we’re sanding down a few rough edges on a cracked foundation—and then holding a press conference about the new paint.

For now, the only responsible stance is cautious optimism wrapped in hard realism: appreciate the help where it’s real, stay clear-eyed about where it’s limited, and refuse to mistake a headline win for a systemic fix. Because the real verdict on this bill won’t be delivered in speeches or rallies—it’s how it feels in a paycheck.

And if you’re wondering where that leaves the growing army of gig workers, freelancers, self-employed hustlers, and small business owners—the people stitching together the modern economy from contracts, side jobs, and 1099s—well, they’re not exactly the stars of this “beautiful” story.

We’ll get to them next. In the following article, I’ll dig into what all of this means for gig economy workers, freelancers, and small businesses—the people who don’t neatly fit into any one category, but who are increasingly the backbone of how work actually gets done.